Shifted-beta-geometric

Implementation of sBG for modeling discrete-time, contractional behaviour. Excel proved to be too difficult for my computer to handle.

import numpy as np

import pandas as pd

import os

from IPython.display import display, Image

from scipy.optimize import minimize

import plotly.graph_objs as go

def compute_probabilities(alpha, beta, num_periods):

'''Compute the probability of a random person churning for each time period'''

p = [alpha / (alpha + beta)]

for t in range(2, num_periods + 1):

p.append((beta+t-2) / (alpha+beta+t-1) * p[t-2])

return p

def pct_dying(data, num_periods):

'''Compute the number of people who churn for each time period'''

n = [1 - data[0]]

for t in range(1, num_periods):

n.append(data[t - 1] - data[t])

return n

def log_likelihood(alpha, beta, data):

'''Objective function that we need to maximize to get best alpha and beta parameters

**Computed log-likelihood will be 1/n smaller than the actual log-likelihood (n = original sample size)**

'''

if alpha <= 0 or beta <= 0:

return -99999

probabilities = np.array(compute_probabilities(alpha, beta, len(data)))

percent_dying = np.array(pct_dying(data, len(data)))

return np.sum(np.log(probabilities) * percent_dying) + data[-1] * np.log(1 - np.sum(probabilities))

def maximize(data):

'''Maximize log-likelihood by searching for best (alpha, beta) combination'''

func = lambda x: -log_likelihood(x[0], x[1], data) # x is a tuple (alpha, beta)

x0 = np.array([100., 100.])

res = minimize(func, x0, method='Nelder-Mead', options={'xtol': 1e-8, 'disp': False})

return res.x

def forecast(data, num_periods):

'''Forecast num_periods from the data using the sBG model'''

alpha, beta = maximize(data)

probabilities = compute_probabilities(alpha, beta, num_periods)

expected_alive = [1 - probabilities[0]]

for t in range(1, num_periods):

expected_alive.append(1 - np.sum(probabilities[0:t+1]))

return pd.Series(expected_alive)

def forecast_dataframe(data, num_periods):

'''Creates dataframe with forecast with additional performance columns'''

forecast_column = forecast(data, num_periods)

actual_column = pd.Series(data)

period = pd.DataFrame({'Period': np.arange(1, np.max([len(data) + 1, num_periods + 1]))})

actual = pd.DataFrame({'Actual': actual_column})

the_forecast = pd.DataFrame({'Forecast': forecast_column})

df = pd.concat([period, actual, the_forecast], axis=1)

# Compute pct error as well

df['pct_error'] = np.abs(df['Actual'] - df['Forecast']) / df['Actual'] * 100

return df

df = pd.read_csv('../data/sBG-1.csv')

df

# Get predictions on 12 periods using 7 periods of data for both segments

regular_series = forecast(df.loc[:7, 'Regular % Alive'].to_list(), 12)

highend_series = forecast(df.loc[:7, 'Highend % Alive'].to_list(), 12)

regular_df = pd.DataFrame({'Year': np.arange(1, 13),

'Expected %': regular_series

})

highend_df = pd.DataFrame({'Year': np.arange(1, 13),

'Expected %': highend_series

})

regular_df = (

df

.loc[:, ['Year', 'Regular', 'Regular % Alive']]

.merge(regular_df, on='Year')

.assign(

Expected=regular_df['Expected %'] * 1000,

pct_error=lambda x: np.abs(x['Expected'] - x['Regular']) / x['Regular'] * 100

)

)

highend_df = (

df

.loc[:, ['Year', 'Highend', 'Highend % Alive']]

.merge(highend_df, on='Year')

.assign(

Expected=highend_df['Expected %'] * 1000,

pct_error=lambda x: np.abs(x['Expected'] - x['Highend']) / x['Highend'] * 100

)

)

regular_df

highend_df

# in-sample, out-sample MAPE

np.mean(regular_df.loc[:7, 'pct_error'].to_list()), np.mean(regular_df.loc[8:, 'pct_error'].to_list())

fig = go.Figure()

fig.add_trace(

go.Scatter(

x=regular_df['Year'],

y=regular_df['Regular'],

mode='lines',

name='Actual'

)

)

fig.add_trace(

go.Scatter(

x=regular_df['Year'],

y=regular_df['Expected'],

mode='lines',

name='Expected'

)

)

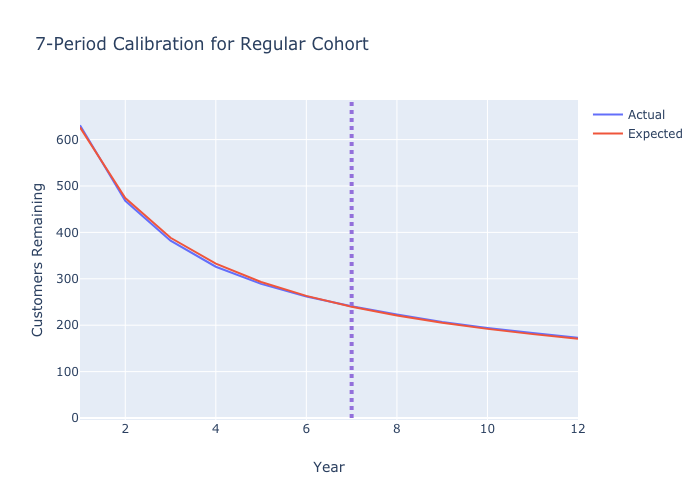

fig.update_layout(title='7-Period Calibration for Regular Cohort',

xaxis_title='Year',

yaxis_title='Customers Remaining',

shapes=[

go.layout.Shape(

type="line",

x0='7',

y0=0,

x1='7',

y1=681,

line=dict(

color="MediumPurple",

width=4,

dash="dot",

))

]

)

fig.show()

Image(filename='../images/sBG-figure-1.png')

fig = go.Figure()

fig.add_trace(

go.Scatter(

x=highend_df['Year'],

y=highend_df['Highend'],

mode='lines',

name='Actual'

)

)

fig.add_trace(

go.Scatter(

x=highend_df['Year'],

y=highend_df['Expected'],

mode='lines',

name='Expected'

)

)

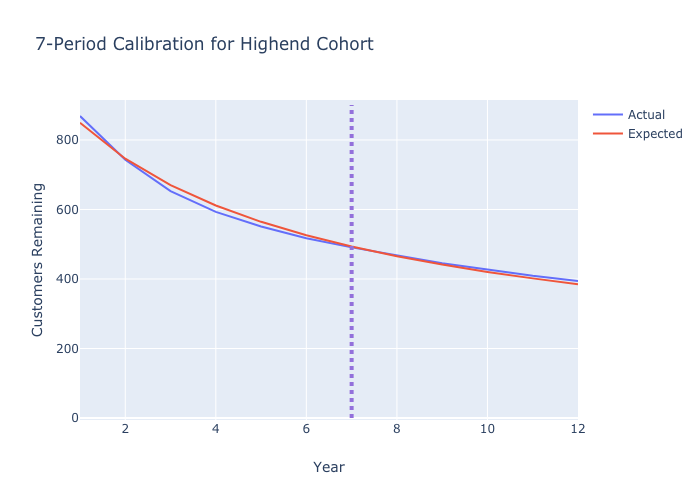

fig.update_layout(title='7-Period Calibration for Highend Cohort',

xaxis_title='Year',

yaxis_title='Customers Remaining',

shapes=[

go.layout.Shape(

type="line",

x0='7',

y0=0,

x1='7',

y1=900,

line=dict(

color="MediumPurple",

width=4,

dash="dot",

))

]

)

fig.show()

Image(filename='../images/sBG-figure-2.png')